We offer this newsletter to provide insight into current information and trends in business and the appraisal industry. We hope you find it enriching and welcome any questions or comments you may have.

For more information about our practice please visit our website at GRWAppraisalServices.com or call us at 5125743444. Enjoy!

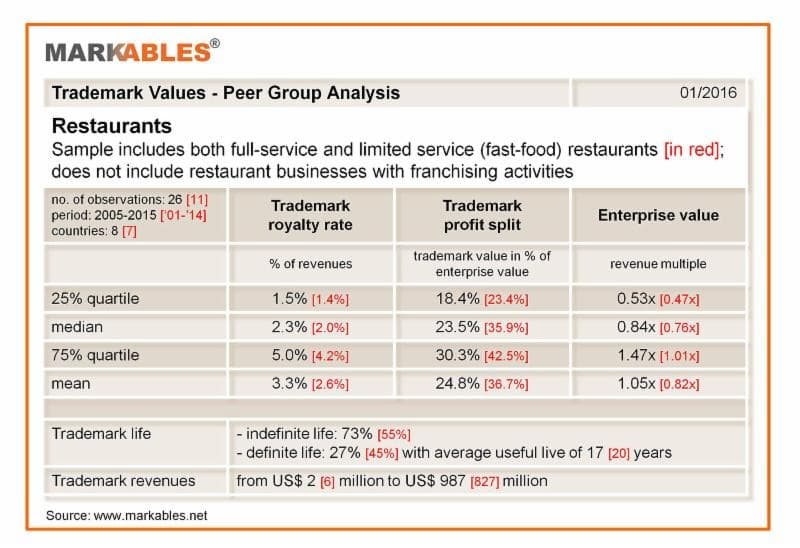

Restaurant brand value multiples keyed to price positioning

When eating out, how important is the restaurant brand? An analysis from Markables, a Switzerland based trademark valuation database, illustrates trademark comparable data for both full service and fast food restaurants (fully owned and operated restaurants only, not franchised operations). Some of the larger restaurant brands in the sample are LongHorn Steakhouse, The Capital Grille, O'Charley's, Yard House, Roman's Macaroni Grill, Mimi's Café, and Einstein Bros. Bagels, among others.

Two key points: The analysis reveals two noteworthy issues. First, restaurant brand value multiples depend on the price positioning of a particular brand. Full service, sitdown restaurants generate a higher brand value premium than fast food restaurants. The same observation can be made within each group. Second, pure play trademark royalty rates must not be confounded with franchise royalty rates, which are most often in the area of 4% to 6% on revenues. As a rule of thumb, the value of the trademark makes up for approximately 50% of the franchise, with the remainder for the operating system, recipes, and trade secrets.

Trademark royalty rates range from 1.5% to 5% on revenues, with median rates of 2.3% for full service and 2.0% for fast food restaurants (see chart). The trademark accounts for about 25% of enterprise value of full service restaurants and 35% for fast food restaurants. Average enterprise value multiples for the sector are 0.85x revenues for full service and 0.75x for fast food restaurants.

How much is a craft brewery worth?

How about a billion dollars? Home brewers who simply want to concoct a great tasting beer for friends and family now have a reason to aim higher. A billion reasons, actually. San Diego's Ballast Point, a craft brewery that got its start in the back of a homebrew supply store in 1992, was bought by alcoholic beverage conglomerate Constellation Brands Inc. The price: $1 billion.

Those aren't beer goggles you're wearing. That staggering amount reflects the frothy market for craft brews, which are steadily outpacing growth of the beer industry as a whole as consumers develop a taste for bold and bitter suds. "It's hard to digest," Bart Watson, chief economist for the national Brewers Assn., said about Ballast Point's price tag. "But it shows where the growth is heading. They're willing to pay a high price because they believe they will see continued growth and a return on investment."

And talk about growth: Ballast Point said beer barrel shipments are set to more than double in 2015, from about 123,000 last year. Revenue nearly $50 million in 2014 is expected to more than double too. The spectacular rise puts that $1 billion in better perspective [say author David Pierson of the Los Angeles Times]. Based on last year's sales, Constellation would be paying 20 times Ballast's revenue, which sounds ridiculous. But 10 times revenue? Not so much. And continued supergrowth through 2016 would make the price seem more reasonable still.

The whole craft beer industry not just Ballast is on a tear, even with overall beer growth in the U.S. nearly flat as the Buds, Millers and Coors of the world lose share and fall out of favor. Barrel shipments for craft brewers rose almost 18% last year, with higher rates to come, according to the Brewers Assn. So the big beer makers are bidding up prices. Heineken bought a 50% stake in Lagunitas Brewing Co. of Petaluma, Calif., MillerCoors acquired San Diego's Saint Archer Brewing Co., and AnheuserBusch InBev's bought Golden Road Brewing of Los Angeles. Based on the Ballast deal, price tags must have been high though none of the companies will say just how much.

The deal certainly had jaws dropping in San Diego, one of America's premier beer towns, home also to Stone, Green Flash and other topnotch beer makers. "The very first guy to walk into my office this morning, the first thing he says to me is, '$1 billion. Are you freaking kidding me?'" said Kevin Hopkins, president of the San Diego Brewers Guild and an employee of Vista Mother Earth Brewing. Even Ballast Point's chief commercial officer, Earl Kight, admitted surprise when confronted with the size of the deal. "I can't believe it either," he said in a phone interview Monday.

The barrage of craftbeer deals reflects a massive shift toward consolidation in the alcohol industry this year as beer behemoths try to capture market share as overall sales growth stagnates. That was perhaps the key motivation behind AnheuserBusch InBev's agreement last month to buy rival SABMiller in a megadeal valued at $110 billion. Craft beer, however, is bucking the trend. Growth is impressive by many measures. Craft's market share for beer in the U.S. grew to 11% in 2014 from 4.9% in 2010. Retail sales of craft beer in 2014 totaled $19.6 billion, up from $8.8 billion in 2010, according to the Brewers Assn. "Per capita spending on alcohol is stagnant in the U.S.," said Nick Petrillo, an analyst for IbisWorld. "Where it's not stagnant is craft beer. It's the reason why the industry's largest macro breweries [are buying craft breweries]. I guarantee going into 2016 it's something we'll see more frequently."

Ballast Point started selling beer commercially in 1996 and has grown into the 31stlargest craft brewer in the country, according to the Brewer's Assn. Ballast Point produces more than 15 kinds of beer yearround, along with seasonal beers and craft spirits, best known for its Sculpin IPA. With Constellation, Ballast Point gets a huge infusion of cash for expansion. Recently, the brewer quashed ITS IPO plans after filing papers last month for an initial public offering. Cheers!

Excerpts from Los Angeles Times November 15, 2015

FASB issues new lease standard; veers from IASB

U.S. companies will be required to add leases to their balance sheets under an overhaul of the lease accounting rules by the FASB. Accounting Standards Update (ASU) No. 201602, Leases, will apply to both capital (aka finance) and operating leases. Up to now, GAAP has required only capital leases to be recognized on lessee balance sheets.

Key impact: Lessees will be required to recognize the value of assets and liabilities on the balance sheet for the rights and obligations created by all leases with terms of more than 12 months. While a company's book value isn't likely to change significantly under the new rule, some financial ratios (e.g., return on assets) could be affected because companies will appear more leveraged.

As under current GAAP, the accounting for a lease primarily will depend on its classification as a capital or operating lease: For capital leases, lessees will recognize amortization of the rightofuse asset separately from interest on the lease liability. For operating leases, lessees will recognize a single total lease expense.

Out of synch: The International Accounting Standards Board (IASB) also recently issued a final lease standard (IFRS 16,Leases) that will require companies to bring leases onto the balance sheet. The January 27 issue of BVWire, and appraisal industry publication, reported that it would not be fully converged with the FASB standard, which is how it panned out. The IASB and FASB agree on many points, including the requirement that all leases of more than 12 months be recognized on lessee balance sheets. But they diverge in some respects, including lease classification. The FASB standard uses a dualreporting model for lessees, while the IASB standard uses a singleclassification model that requires lessees to account for all leases as capital (finance) leases. The FASB standard will take effect for public companies for fiscal years, and interim periods within those fiscal years, beginning after Dec. 15, 2018. For all other organizations, the ASU on leases will take effect for fiscal years beginning after Dec. 15, 2019, and for interim periods within fiscal years beginning after Dec. 15, 2020. Early application will be permitted for all organizations.

Article from BV Wire March 2, 2016

Record prices, low capitalization rates for skilled nursing/assisted living

Lower observed capitalization rates indicate higher prices. After a recordsetting year across all senior care sectors in 2014, average skilled nursing facility prices soared again to a new record of $85,900 per bed, or 12% higher than in 2014, according to a soontobe published study from Irving Levin Associates, The Senior Care Acquisition Report, 21st edition, 2016.

In the assisted living market, the average price paid per unit just topped the previous record set in 2014 by less than 1.0%, reaching $189,200 per unit in 2015. Average skilled nursing capitalization rates dropped to 12.2%, just 10 basis points above their record low, and assisted living cap rates stayed the same as in 2014 at 7.7%.

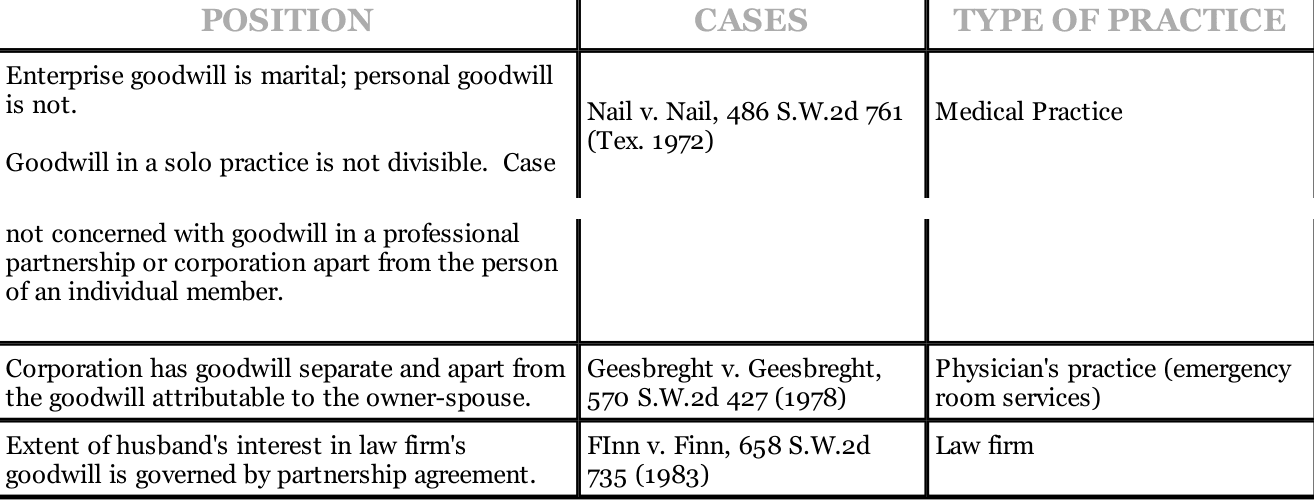

State-by-state court case chart on goodwill updated

BVR, an appraisal industry information provider, has just updated its everpopular complimentary download formerly titled "Goodwill Hunting in Divorce." It gives you an at aglance look at a state's basic position toward enterprise and professional goodwill so that you can shape your valuations accordingly. Below we present positions taken in Texas courts.

Expanded info: The updated chart has a new title, "Charting Goodwill Jurisprudence," to reflect an expanded discussion of the law that includes excerpts from foundational cases that highlight the concepts (e.g., salability, transferability, solo practice, noncompete agreements) underlying a state's position. Additional information gives insight into how different courts emphasize different concepts and how much discussion there is within a jurisdiction around the basic rule.

The complete chart can be found at http://www.bvlibrary.com/.

GRWAppraisalServices.com*512.574.3444*GRWAppraisal@gmail.com