I offer this newsletter to provide insight into current information and trends in business and the appraisal industry. I hope you find it enriching and welcome any questions or comments you may have. If there is a topic you'd like me to discuss or report upon let me know.

We provide services including business valuation, divorce consulting, litigation support, forensic accounting, transaction due diligence, and operations consulting. For further information about our practice please visit GRWAppraisalServices.com. You may email me at GRWAppraisal@Gmail.com or call me directly at 512574 3444. Enjoy! Greg Weichbrodt Principal

This writing presents a publication that may be useful in the valuation of law firms, additional considerations of valuation standards, and an opinion on automated valuation models.

The valuation of law firms

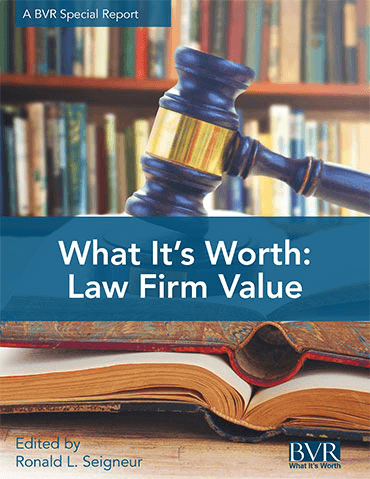

There is a new publication about the valuation of law firms. It is the special report published January 2017 by Business Valuation Resources (BVR), What it's Worth: Law Firm Value. It provides a foundation for determining law firm value and offers law firm owners advise on succession planning.

Highlights of the report include:

- An overview of the methodologies used, the special considerations to take into account, and a useful checklist of questions to consider when performing a law firm valuation

- Direction on key value drivers for law firms with current market information

- Summaries of the latest benchmarking data and valuation rules of thumb

- An overview of the the excess earnings method to value the goodwill of a law firm with a comprehensive case study

- A look at how the courts ruled on key aspects of law firm valuation with 11 important court cases where law firm value was front and center

- Advice on succession planning for law firm clients and owners

- A sample law firm valuation report, which gives you insight into the work product that can be expected when an appraiser opines on the value of a law firm

This report may be a good starting point for law firm partners looking to understand the primary factors considered in determining the value of their equity stake.

Further discussion on applied standards of value

In our Winter 2017 edition of Firm Values, I wrote about nuances of two regularly applied valuation standards: 1) fair value and 2) fair market value. A recent conversation with a fellow valuation practitioner gave me the opportunity to reflect on the selection of the appropriate standard or methodology applied in a given situation. While the applied standard may be dictated by statute or determined by the court, there may be other factors that lead to an alternative value conclusion.

While my buddy and I were on a recent motorcycle ride through the Texas Hill Country, I received a call from my appraisal cohort, John. John, informed me he was the appraisal expert in a marital dissolution matter. His assignment was to opine on the value of three minority interests. His client was the spouse of a doctor. The doctor was a small shareholder in several medical practices. John informed me that he thought that his assignment was clear cut, but was uneasy with the potential that he may have missed something.

In order to decide on the appropriate methodology to use in valuing the subject interests, he turned to the language in the medical practice partnership agreements. Many partnership agreements have language that explicitly state whether fair value, fair market value, or some other standard should prevail. Each of the agreements was clear in the case of divorce. Each dictated that under such circumstance, the selling partner was to receive the unadjusted net book value of the partner's equity. On its face it seemed apparent that John's job would be a simple accounting exercise but before deciding to rely upon the partnership agreement language, two thoughts came to mind.

First, since the doctor held a small minority interest in three medical practices, I asked John if he considered how she gained ownership of the interests. Did the doctor buy into the practices at amounts that included value not identified on the books? In other words, did the doctor's capital accounts capture the total values of the doctor's interests in the practices? Or, did the capital accounts consist of something less than the amount paid for the interests? Were moneys withdrawn by a departing doctor, or was some other component of value, such as goodwill netted against or not recorded in the doctors capital account? These questions address whether an equitable division of assets would take place if the appraisal method directed by the partnership agreement was utilized. Was there consistency in value methodologies between how the ownership interest was obtained and how it would be sold?

Second, I asked John if there had been any other transactions in interests in the subject medical practices. If so, were these interests transferred at values other than net book value? If so, were there legitimate reasons for such differences in value methodologies? Regardless of the explicit language in a partnership agreement, it may be the case that the partners have acted or intended to act contrary to the partnership agreement. After all, a partnership agreement is a document that is meant to reduce to writing, the will of the parties. When it comes down to crunch time, was it relied upon?

Ultimately, it is important to take a methodical look at the total picture of the subject transaction, in context with previous actions of interested parties, intentions of such parties, and what is equitable between the parties in a divorce. John and I agreed that it would be good to discuss the alternative considerations with his client's attorney and come to an agreement on a proper course of action. Perhaps making a value determination by assuming alternate facts may provide a reasonable settlement alternative to a trier of fact. John and I hung up. I strapped on my helmet and continued my ride.

Lost Maples State Natural Area

Automation not at its finest

This may sound like it came from the lips of commentator Frank Deford, but here it is. I recently took an automated business valuation application on the Web for a test ride (to continue the motorcycle theme). The application offers to provide an immediate appraisal conclusion of your business with a few key strokes. I began by entering my hypothetical business name and its latest annual revenues. The application provided an appraisal estimate immediately. I was disappointed. I thought the valuation would be higher. Like TurboTax and tax refund amounts (or in my case, amounts owed), my valuation number recalculated with every input. I plugged in my revenues, pretax earnings, balance sheet data, and answered five or so questions about my business and that was it. I received my custom valuation assessment in minutes.

As you may have guessed, at best, I don't think these models are anything but a novelty and at worst, a business owner may place reliance upon the output generated by such an application and actually make a business decision based on it. I read the sample report. Within the general text of the report is the following disclaimer: "Some events and circumstances that might impact the overall valuation of a specific business may not be taken into account for the purpose of this report." I translate this to mean don't rely upon this valuation report. In fact, to their credit, the report disclaimer continues: "It's important to note that the estimates presented herein are not "final numbers." Instead, we are providing general estimates. As a result, the overall valuation should be considered a frame of reference and not an official appraisal." A general calculation of value may provide a starting point for a curious business owner. Though, without full consideration of all relevant facts, I cannot think of a helpful purpose under important circumstances. The websites hidden disclaimer is much more clear on the limitations of their product. It states: "We hope [our report] is of interest to you. But you should not rely on them for any specific action." and "You may not use the information for any commercial purpose".

Aside from business owners, the website markets it services to accountants, business analysts, and bankers. The widespread use of such a model could cause a real problem for equity markets or the vast pool of baby boomers now retiring. Now, consulting professionals are encouraged to utilize a novelty item under the shroud of providing a legitimate service to their clients. Remember the banking disaster and Great Recession that originated from faulty real estate appraisals? How is this different? Are the equity markets next? It took me nearly a decade of learning and practicing my craft to develop a satisfactory level of comfort in presenting my appraisal conclusions to my clients. This work cannot be reduced to a simple algorithm. Four important inclusions in a sound valuation process that are absent from an automated appraisal application include:

A site visit Don't have your business appraised by an out of state practitioner known only through email, or telephone, or worse, a few keystroke into a web page. Each time I visit a company I meet face to face with and speak to the owner. I leave with a more complete understanding of the quality of management and the nature of operations. Insight into the existence and condition of reported fixed assets is gained. Operating strengths and weaknesses are better understood.

A period of reflection I ask for a minimum of a week's time from when I receive the requested documents to perform my appraisal analysis. I do so because inevitably, there are factors that come to light only after a diligent look into the detail of the financial information, and a back and forth discussion with management.

A management interview After all, management knows the most about the business. An inspection of a company's financials always leads to questions about income patterns, expense items, or otherwise. Asking open ended questions helps in learning unanticipated critical information about a business.

Transparency The inclusion of critical underlying information, such as: 1) guideline industry financial data, 2) company transaction pricing data, 3) income approach, market approach, and assetbased approach methodology calculations, 4) cost of capital development calculations, 5) key value driver explanations and reasons behind certain decision points all lead to a clearer understanding of a value determination for readers of an appraisal report. Providing such information allows the recipient to recreate the the appraisal calculations and perhaps perform sensitivity analyses on the inputs so they may understand how certain factors effect value.

Ultimately I believe in the tried and true, thorough and thoughtful analysis of company information, use of professional insight, and input of management in developing a useful tool with which a business owner can make critical decisions. There is no substitute, however fun it may be to see the valuation number change like a carnival scale. Thanks for the inspiration Frank.

GRWAppraisalServices.com*512.574.3444*GRWAppraisal@gmail.com

GRW Appraisal Services, 8401 Lone Mesa, Austin, TX 78759